If 2024 was the year of Elections, Economics, Evolutions and Earnings, what is in store for Australian equities in 2025?

The year 2024 proved to be a remarkable one, both in absolute terms and relative to expectations. As the year unfolded, it brought numerous surprises and developments that shaped the global economic and political landscape. From election outcomes (and associated geopolitics), diverging economic growth (and interest rate changes), to the AI evolution (and associated ripple effects) and finally the return of earnings revisions as a key relative individual stock performance driver.

Elections, economics, evolutions and earnings – a fitting summary of some of the primary forces behind the global equity rally as 2024 draws to a close.

Below we explore these themes in more detail, share our outlook for 2025 and how the Alphinity Australian Funds are positioned going into the New Year.

2024 in review:

As we entered 2024 a year ago, there were widespread expectations of significant rate cuts in the United States. However, as the year progressed, only a handful materialised, accompanied by a soft landing for the economy. In Australia, the Reserve Bank maintained a resolute stance against rate cuts, though some cracks in this position began to appear towards the year’s end.

The U.S. presidential election was a focal point of 2024, filled with twists and turns. The outcome, with Donald Trump’s victory, is likely to usher in policies and a political and regulatory environment perceived as pro-business and pro-market. Meanwhile, China’s

attempts at economic stimulus, while showing some much-needed strong intent, fell short of expectations in the detail, failing to provide the anticipated boost to global growth just yet.

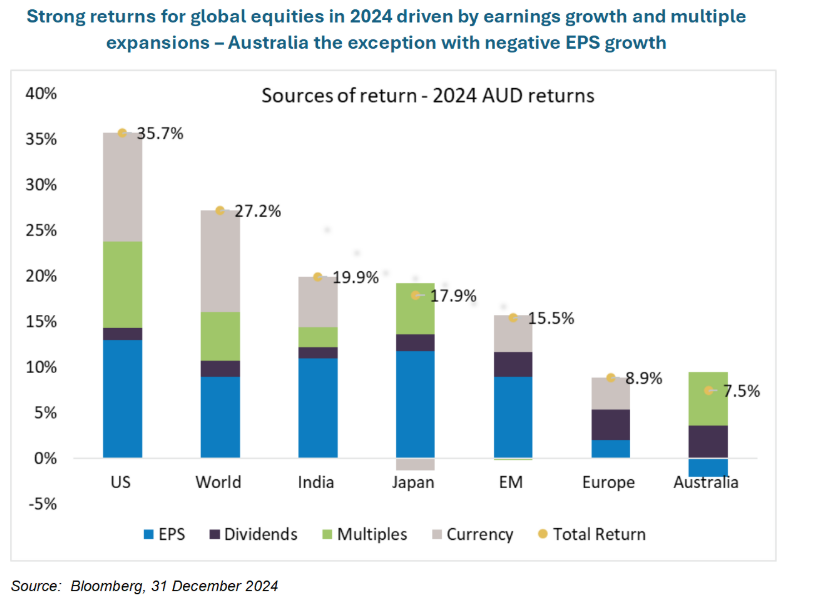

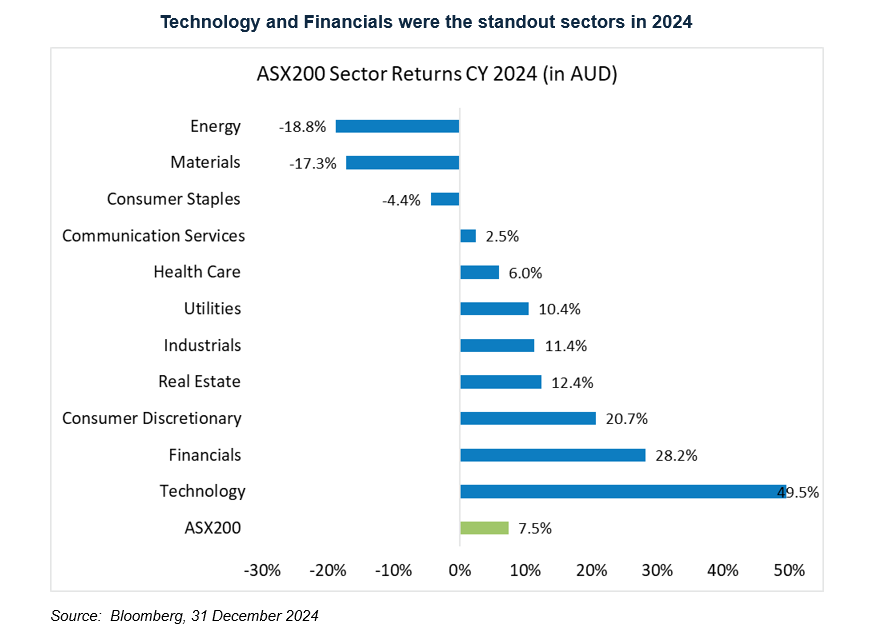

In the financial markets, the U.S. stock indices continued their upward trajectory, propelled by the “Magnificent Seven” tech giants and artificial intelligence advancements. This momentum had a positive spillover effect on the Australian market, with the technology sector the highest contributor to returns despite the pullback in December (+49% YTD). Outside of the tech sector, the strong performance in the US had a broader positive impact in the Australian market through the year, despite quite different economic and earnings outcomes.

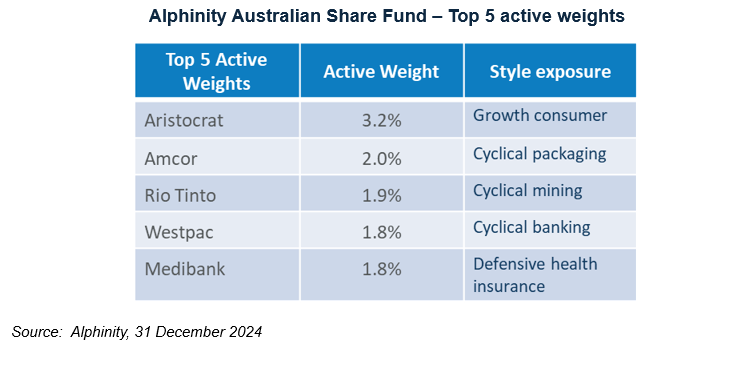

For Australian investors, the strength of major banks, particularly Commonwealth Bank and Westpac, was also noteworthy, driven by small but persistent earnings upgrades. With earnings upgrades few and far between elsewhere (the market in total having net downgrades), financials continued to be well supported, almost regardless of valuations.

From a portfolio and process perspective, it was encouraging to see the re-emergence of earnings revisions as a key individual stock driver and alpha generator over the last 12 months, something that went temporarily missing for much of 2022 and 2023 as large top down thematics and swings took precedence. This trend allowed for consistent momentum to be a key driver, which assisted all the Alphinity funds to capture positive alpha for our clients this year.

The outlook for 2025:

Looking ahead to 2025, the outlook appears more nuanced. A repeat of the robust absolute returns seen in 2024 seems less likely, given the high valuations and elevated expectations that now form a more challenging starting point. Unlike 12 months ago, everyone appears positioned for a “no-landing” or at worst a “soft-landing” already, with very little wall-of-worry to climb. However, a precipitous decline is not anticipated either. Several positive factors remain that could continue to drive the market forward.

The U.S. economy continues to show resilience, and the new Trump administration is expected to implement pro-business, growth-oriented policies and a market friendly environment, at least initially. There’s potential for more rate cuts in international markets (even though less than hoped for initially) including, but perhaps toto a lesser extent, in Australia. China, while still facing challenges, has demonstrated strong intent and retains some levers to stabilise its economy, potentially becoming less of a drag on global growth and sentiment. We have our own election here in Australia that is likely to lead to more fiscal stimulus promises from the major parties, and a focus on ‘cost-of-living’ pressures.

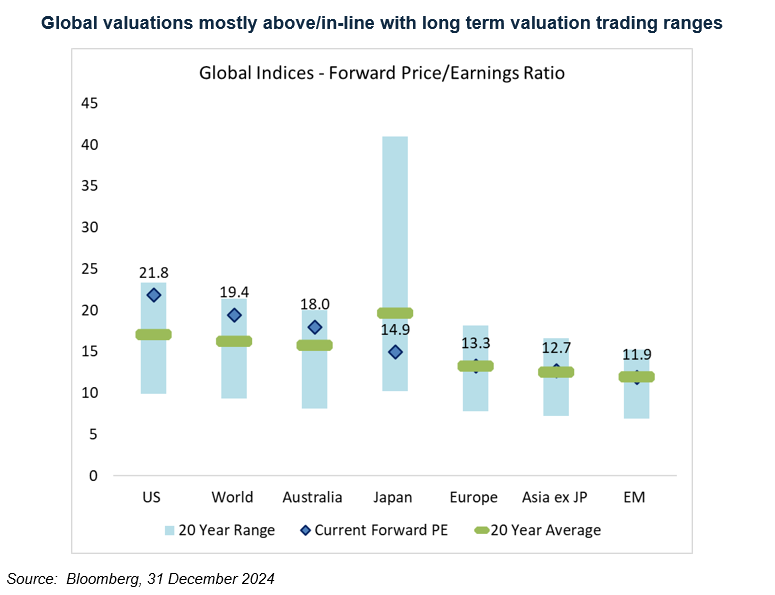

Nevertheless, earnings expectations in the U.S. are already quite high, (less so here in Australia), making further PE expansion as the main market driver less likely unless we have a material change in interest rate view. The focus will need to shift to actual earnings outcomes. Uncertainties surrounding U.S. trade policies, inflation trajectories, interest rate movements, and geopolitical tensions add complexity to the outlook.

While material growth in market indices may be harder to achieve in 2025, there is enough positive momentum to sustain current levels for some time. A period of market consolidation wouldn’t be surprising however after the strong run in 2024, though a more significant correction would likely require catalysts beyond just high valuations (such as an economic, earnings or interest rate policy surprise).

It is likely that rather than the level of the market, the key question for 2025 will revolve around potential sector and stock rotation. Will the current market leaders maintain their dominance, or will we see new market leadership emerge? For example, changes in monetary policy, such as rate cuts in Australia, could benefit domestic and consumer cyclical stocks. A recovery in China or more forceful policy might boost commodities, as would improved US and global economic growth. In a flatter or weaker market environment, defensive stocks might get their time in the sun yet again. Ultimately, whatever the market environment it is likely to be earnings driven. Market leadership will be driven by those companies that can produce better earnings outcomes than expected, which is what we saw eventuate in 2024. The key will be the flexibility to move to where earnings leadership is as the year unfolds.

How are we positioned?

Given these considerations, a relatively balanced portfolio approach seems prudent to start 2025, focusing on likely earnings outcomes in individual stocks rather than trying to second guess broader macro drivers. Some increased defensive positioning is likely advisable due to high market valuations, but maintaining some exposure to domestic interest rate-sensitive sectors could be beneficial for example if rates decrease.

Our portfolios continue to be positioned in stocks with better earnings outlooks than the market expects, as per our investment process. While we do focus on earnings momentum and the quality of those earnings primarily, we also care about valuation. Valuation rarely tells you when a stock or market is going to turn, but it does tell you when risk is increasing. As such, without a better earnings outlook for the market overall, risks in the market have by definition increased alongside those higher valuations. So, the portfolio needs to be very vigilant around investing in stocks that are showing earnings leadership and delivering earnings upgrades.

As the year unfolds and new earnings trends become clearer, we will continue to adjust our portfolios to align with new earnings leaders.