Reflecting on 1Q21 earnings season – Hitting many records

In this paper we reflect on what was one of the best reporting seasons on record – not just due to the number of companies beating expectations, or the sheer size of the beats, but also because of the scale of upward revisions to forward consensus for both 2021 and 2022 earnings.

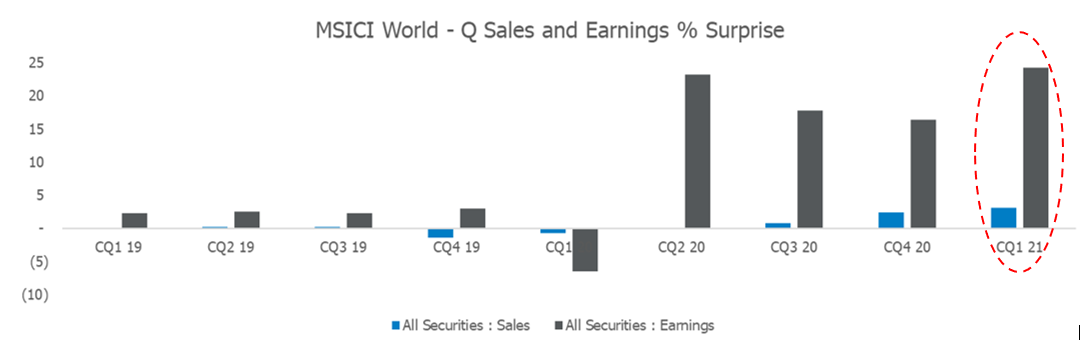

Of the 92% of MSCI World Index companies that have reported to date, a whopping 65% have beaten on earnings (by 24% on average) and 64% on sales. The U.S. has had a particularly strong reporting season, with 87% of the 468 companies (of the S&P 500) that have reported to date beating consensus earnings, whilst circa 60% of European companies have also beaten (by 40% – the highest margin on record). It’s interesting to note that a similar percentage of value and growth companies have beaten earnings expectations. Across sectors, Financials, Communications and Consumer Discretionary have posted the broadest beats so far.

Key themes that have emerged during the reporting season included cost pressure concerns – from raw materials to labour (interestingly not yet very evident in margin pressures), supply chain shortages, concerns around inflation, improved confidence and higher capital expenditure spending plans and finally also the return of dividends/buybacks.

MSCI World – Quarterly reporting season % EPS and sales surprises

Source: Bloomberg

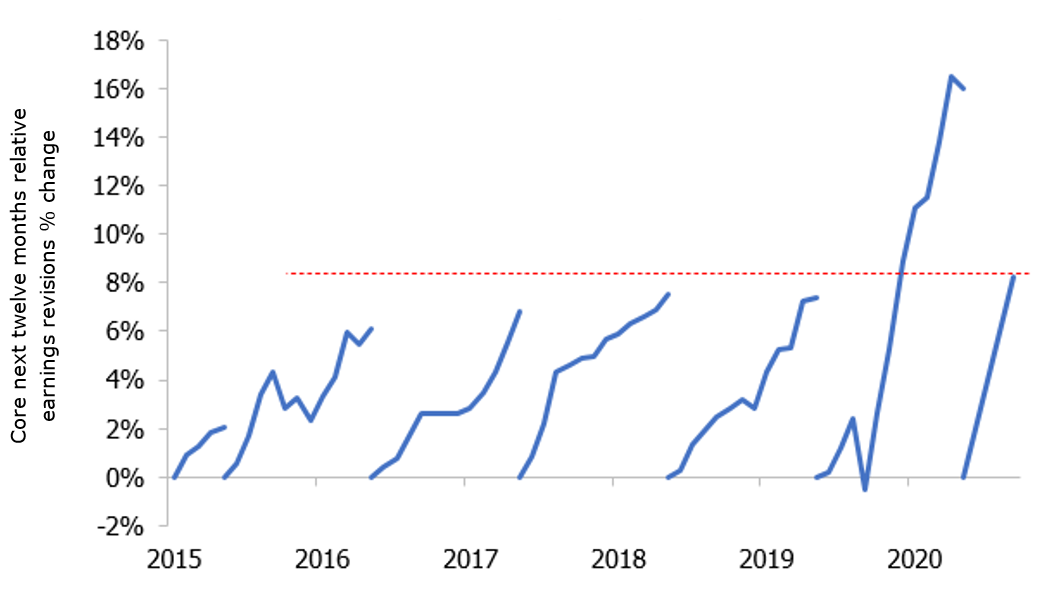

Earnings revisions/trends – Cyclicals still the winners

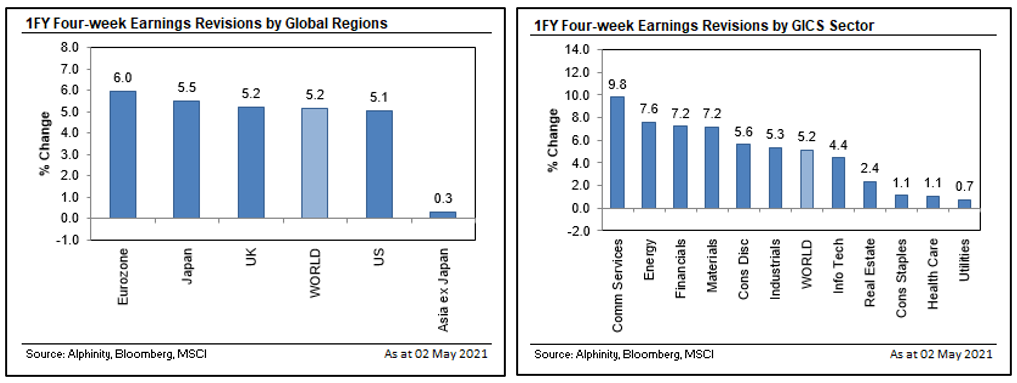

The strong economic rebound and optimism around vaccination progress and ongoing government stimulus (despite bond yields and inflation expectations edging higher) have continued to play out in higher earnings expectations, with material upgrades seen over the past four weeks and three months, and also across all regions with the exception of Asia ex-Japan. Looking ahead, consensus is now expecting earnings growth of +36% for the MSCI World Index in 2021, +12% during 2022 and +9% during 2023.

Interestingly, whilst positive earnings revisions have been relatively even across most regions over the past four weeks, earnings leadership by sector has been much narrower, focused mainly within cyclical sectors, with defensive sectors lagging.

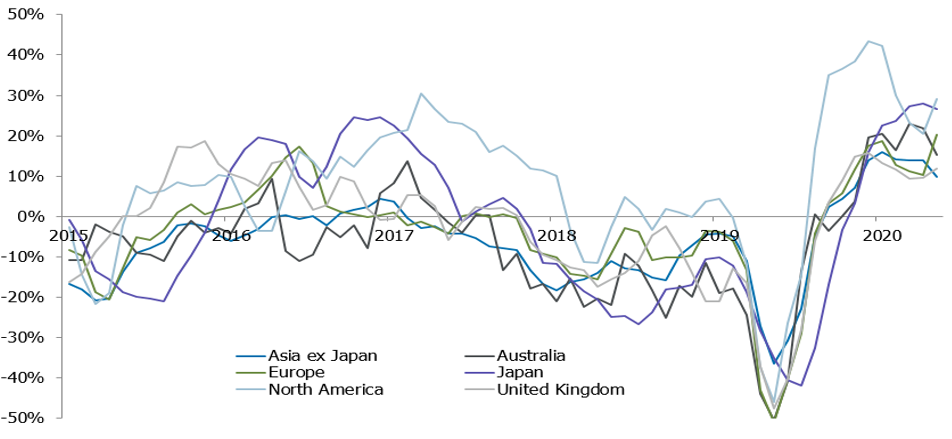

The breadth of earnings revisions (net % of earnings analysts upgrades or downgrades over three months divided by the overall number of analyst estimates), has however also recently slowed in certain markets like the US, but is still accelerating in markets like Europe and here in Australia.

Regional 3-month Breadth of Earnings Revisions

Source: Alphinity, Bloomberg

Market reaction – optimism already priced

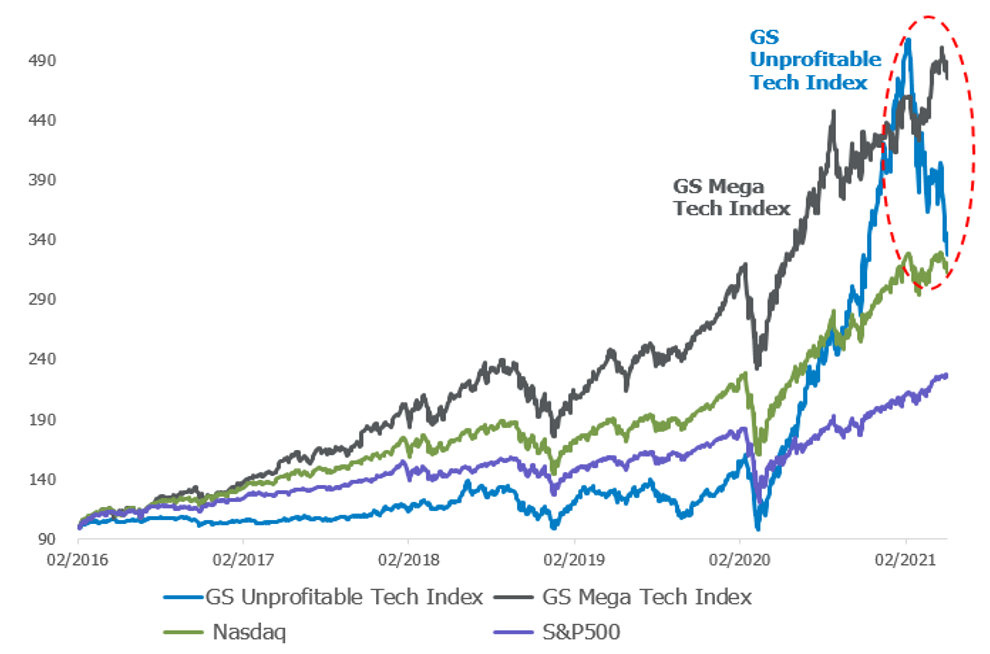

Despite all the optimism around earnings, the price reaction to beats has generally been fairly muted, with misses punished, particularly in sectors such as commodities. Low quality companies bore the brunt of the selling, although even high-quality companies such as some of the FAANG stocks (like Facebook and Amazon) also sold off despite extremely strong results.

Another reminder that the market is forward looking, with high valuations already reflecting a lot of hope about a cyclical earnings recovery.

Historic Performance (USD)

Source: Bloomberg, GS Data

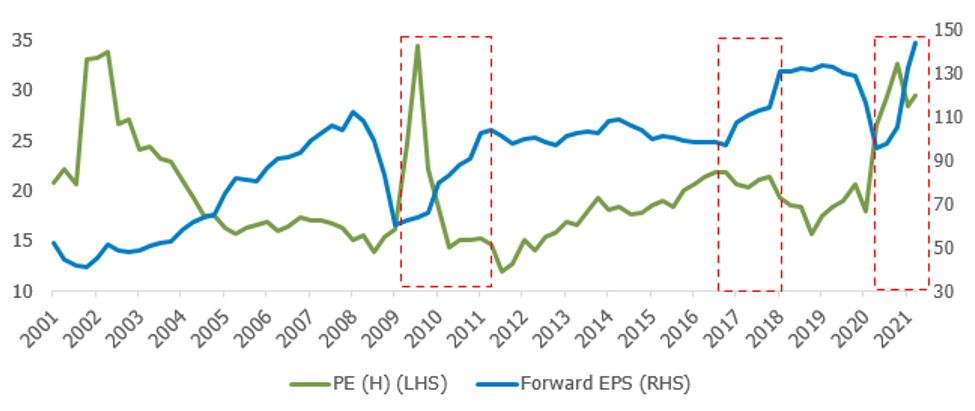

Putting it in perspective – Not all that different to past cycles

MSCI World earnings are now back at pre-Covid levels, with the recent strong reporting seasons cementing a strong rebound from the earnings trough in 2020. Comparing actual Earnings Per Share (EPS) performance in year one of the earnings recovery since the 70’s, the current experience is very similar.

Historically, EPS has risen by an average of +36% in the first year of a recovery, and +23% in the second, which compares to current expectations of 36% and 12% respectively. During this part of the market cycle, earnings growth normally drives performance, and multiples compress, following Price-to-Earnings ratio expansion in the initial ‘hope’ phase of the market rally (which we experienced last year). So, despite this earnings cycle being characterized by super-low interest rates and unprecedented government stimulus, the current earnings/performance trends are playing out much the same as in past cycles.

MSCI World (USD)

Source: Bloomberg

Alphinity Global Equity Fund – Active ETF portfolio – Enjoying above market earnings

Alphinity Global had a particularly strong 1Q21 earnings season, with most of the companies in our portfolio beating expectations by a big margin. This is reflected in our portfolio’s 2021 relative earnings revisions to the market, which is already in line with relative beats we would normally expect for a full year.

EPS Revisions – Alphinity Global vs Market

Source: Bloomberg, Alphinity

Of the 27 companies in our Global Equity Portfolio that have reported 1Q21 results to date, 12 have beaten earnings expectations by more than 20%. Some of the standout results with a 60% plus beat included Amazon, Trane Technologies, Target and Alphabet. Other stand out results – notably across a range of sectors – included ASML, Blackstone, Morgan Stanley, Bank of America, Target and Danaher. Below we explore some of these names in a bit more detail.

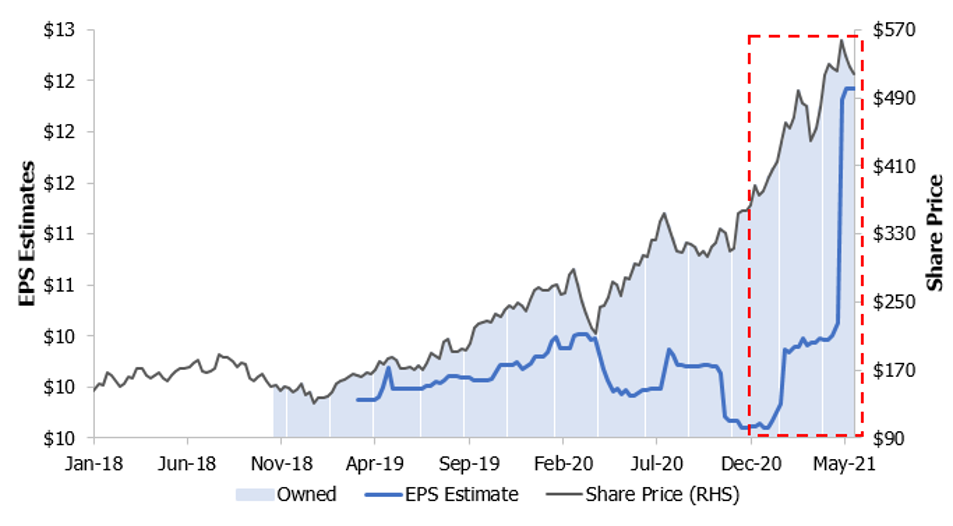

Target (TGT US) – Gaining market share with digitalization

1Q21 result: Target reported a fantastic 1Q result with adjusted 1Q earnings up 525% year-on-year (yoy) and sales up 23%. Comparable store sales grew 23%, store footprint grew 18%, indicating market share gains across varied categories, and comparable digital sales jumped 50%! The retailer also guided to wider 2021 margins than it had foreseen earlier this year, boosted by a shift in demand toward more profitable items like apparel and home decor. Importantly, the company now expects ‘positive single-digit comparable sales growth in the last two quarters of the year, and expects its full-year operating margin rate will be well above the 2020 rate of 7%, with the potential to reach 8% or somewhat higher’.

Our view: Target’s strategy to utilise its store portfolio to deliver an omnichannel experience for its customers has largely now proven itself to the sceptics. The digital fulfilment offerings of ‘click and collect drive up’ and ship subscription, are all lower cost fulfilment options which are highly effective in creating a positive, valued, convenient customer proposition given the national chain and closeness of stores to consumers. Target is also a good company to own if inflation inflects higher, with a strong private label offering and an ability to pass on inflation to its customers, both likely to support comparable sales growth and gross profits. Target has recently demonstrated its ability to increase wages, while still managing cost inflation comfortably.

Target Corp – Forecast EPS Trends (USD)

Source: Bloomberg, Alphinity

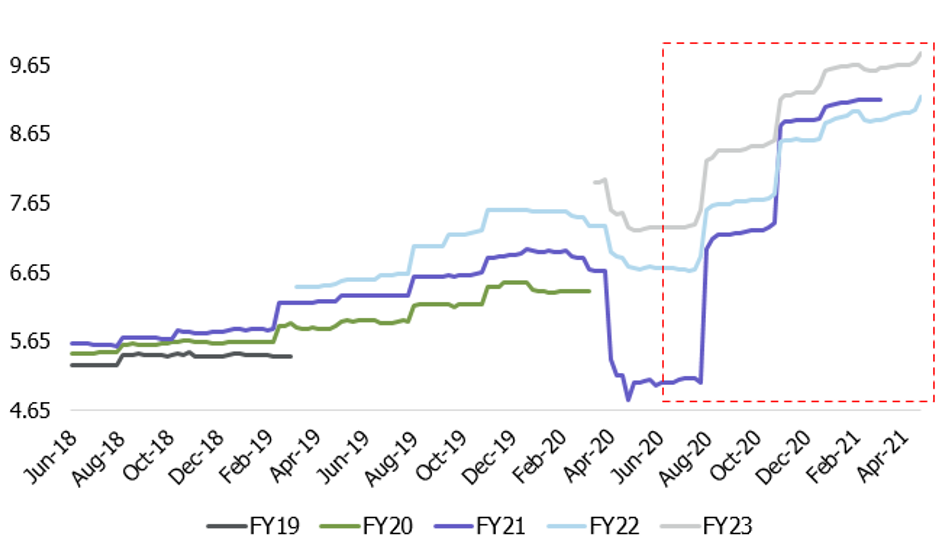

ASML (ASML NA) – Understated manufacturer at the forefront of digital transformation

1Q21 Result: ASML reported a blow-out 1Q21 quarter, beating both earnings and revenue expectations by a significant margin and significantly upgraded FY21 guidance (sales up from circa 13% to circa 30%) as customers rushed to upgrade machines to circumvent the chip shortage. Sales rose 79% yoy during 1Q and profits more than tripled yoy! The semiconductor industry has recently benefitted from explosive demand, and some analysts are now predicting a semiconductor super cycle. Unsurprisingly, ASML’s business has been firing on all cylinders.

Our view: ASML is an exceptional business, at the forefront of digital transformation, providing the machines to help build the chips that will underpin the accelerating adoption of Artificial Intelligence and Internet of Things, with applications including smart homes, smart industry, connected wearables, self-driving cars, mixed reality etc. The metrics the business generates are exceptional, with cash flow return on invested capital (ROIC)>25%, return on equity (ROE)>25%, ROIC>20% and gross margins of 47% in 2020. In our view, these metrics will improve further as growth continues in 2021.

ASML – a significant step change in earnings expectations

Source: Bloomberg, Alphinity

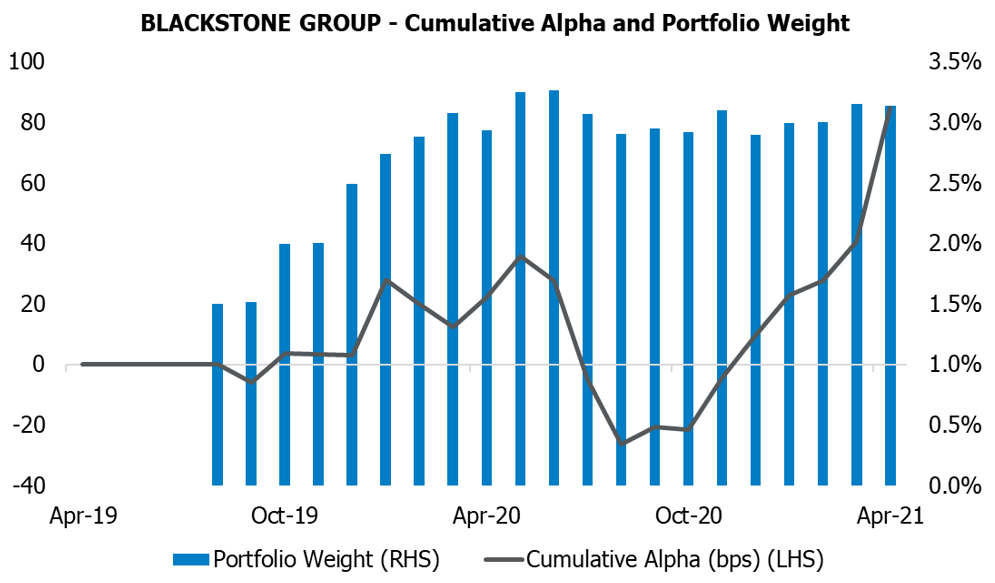

Blackstone (BX US) – A rare kind of gem

1Q21 Result: Blackstone reported very strong 1Q21 numbers across the board, with both sales and earnings comfortably beating consensus expectations, driving subsequent upgrades across assets under management (AUM), inflows, realisations, deployment, fee related earnings and more. Fee related earnings (FRE) jumped 58% and margins increase by 590bps to 54.9%. AUM increased by 21% yoy to $649 billion (ahead of estimates of $637 billion) with a good performance across all strategies and the underlying strength in various new product innovations inflecting higher.

Our view: BX is a best-in-class alternative asset manager and the leading brand in alternative investments, a reputation earned by a combination of successful investments, strong performance, lofty fundraising, and elevated shareholder returns. BX’s diversified AUM base provides unrivalled scale and operating leverage, while its high permanent capital vehicles (so-called ‘perpetual capital’ represents circa 23% of total AUM) reducing earnings volatility and enhancing long term earnings visibility.

BX – adding increasing alpha

Source: Bloomberg, Alphinity

Author: Elfreda Jonker, Client Portfolio Manager

Find out more

For more information, please contact your financial adviser, call the Fidante Partners Investor Services team on +61 13 51 53