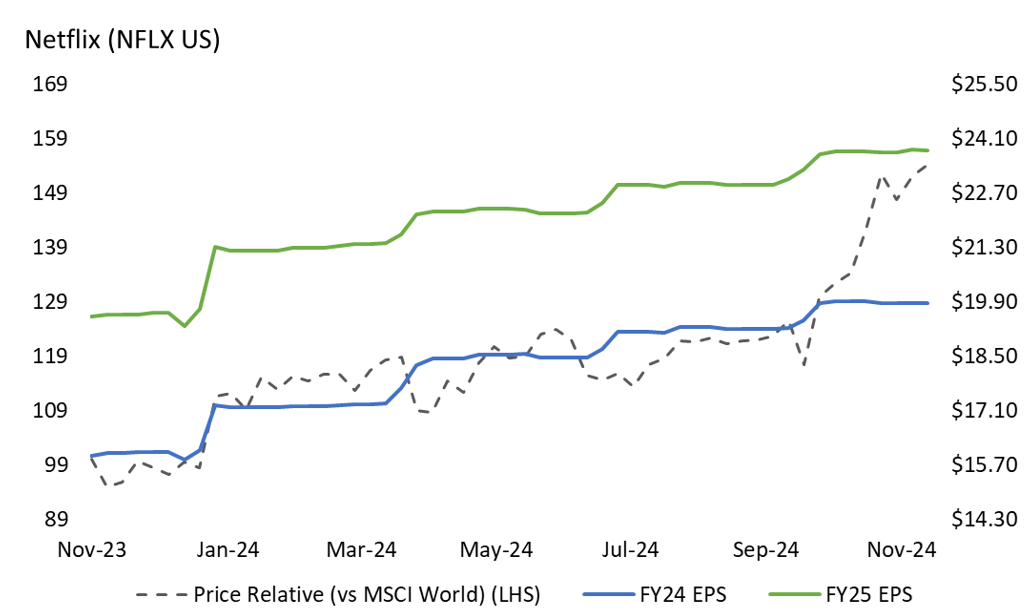

Netflix (NASDAQ: NFLX) has delivered strong performance recently with the share price rising approximately 95% over the last 12 months, outperforming the MSCI World index by around 60%. As a core portfolio holding, it’s timely to explore the driving forces behind the move, and why we believe there is further upside to earnings estimates ahead.

What is driving the stock price?

Three primary factors are driving the strong share price performance: a widening competitive lead, an improving financial profile with additional revenue sources, and a strong content slate.

1) Widening competitive lead

In 2019 Disney launched Disney+, amassing 100m subscribers within three years to challenge Netflix’s dominance. In 2022 Netflix faced its first quarterly subscriber decline since 2011, and it appeared to be the beginning of the end. Fast forward to today and Netflix is arguably in its strongest ever competitive position.

Following a period of heavy investment to build out competing services, peers are pulling back spend to focus on profitability. Disney announced an annualised reduction of $4.5bn on content spending. Meanwhile, Comcast’s Peacock ended its “Free as a bird” strategy in 2023, which provided a free basic tier and placed an emphasis on advertising revenue and has since announced two price hikes as it battles profitability.

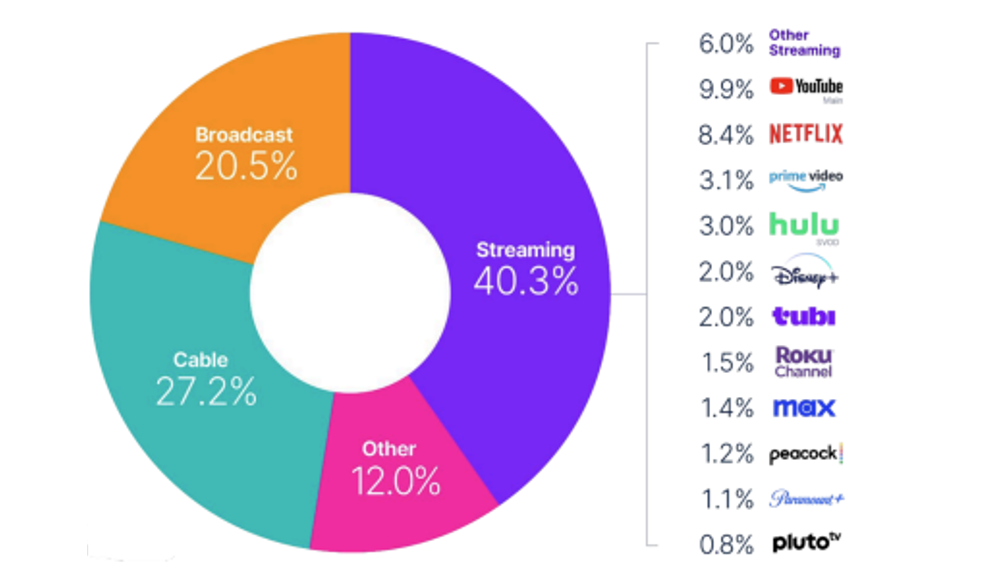

With Netflix spending the most on content by a meaningful margin (estimated to be $17bn this year), and peers forced to retreat and even license product to Netflix in some instances, it provides a stronger customer proposition to expand the content library and drive engagement. Versus other streaming platforms, Netflix commands a higher share of US screen time than the next three competitors combined.

Nielsen’s The Gauge: Share of US TV Screen Time (Total Day – Persons 2+, June 2024

2) Improving financial profile with additional revenue sources

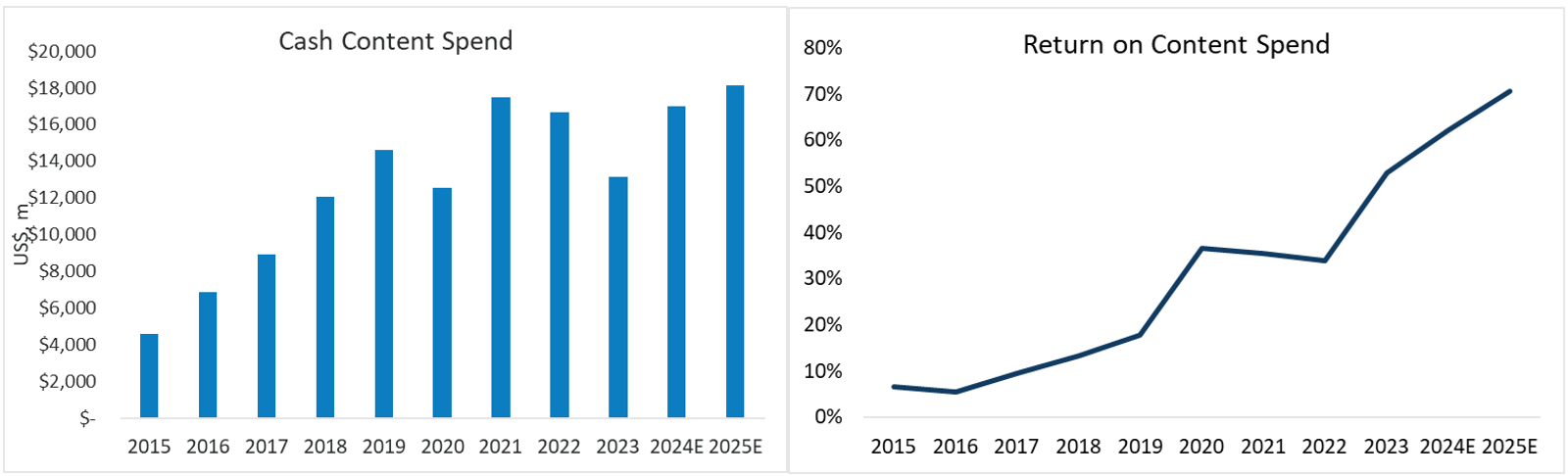

Against the backdrop of peers’ cutting costs, Netflix will continue to increase content spend, but at a slower pace than history as it hits a point of critical scale. As operating income grows, the return on content spend rises from an already impressive level.

Netflix is also growing an ad-supported tier in select markets which currently has an estimated 70m monthly active users. The new tier is priced lower than existing offerings and helps attract members in more economically sensitive geographies, while also opening a new revenue stream from advertising which is growing rapidly.

The benefits of widening the competitive moat, capturing additional revenue sources, and improving the financial profile can be seen in the earnings acceleration below. Following an impressive year in 2024, we estimate that earnings can grow comfortably above 20% in 2025.

3) Strong content slate

Netflix recently dipped a toe into live sports with the Mike Tyson vs Jake Paul boxing match which peaked at 65m concurrent streams. The Katie Taylor vs Amanda Serrano match beforehand became the most watched professional women’s sports event in U.S. history with 50m households tuning in. On a pay-per-view basis this could have cost $50, but Netflix included this for free within its membership.

The broadcast was not without its hiccups (I’m not sure viewers tuned in to see Mike Tyson’s backside) but broadly speaking was a triumph and shone light on Netflix’s capability to handle large events and scale them to a global audience. This power of the platform was showcased to members (included for free within existing membership), sporting franchises, and advertisers (both benefiting from a global audience not available elsewhere).

Netflix intends to retain newfound members with a strong lineup of content such as the NFL Christmas Day games (featuring Beyonce as the halftime entertainment), Squid Game 2, and the finale of Stranger Things. Collectively the lineup positions Netflix to drive further member engagement in the coming quarters.

Further earnings upside ahead

In addition to the strong content rollout growing the subscriber base and reducing churn, there are two primary levers for Netflix to continue beating earnings estimates: latent pricing power and operating expense control.

1) Latent pricing power

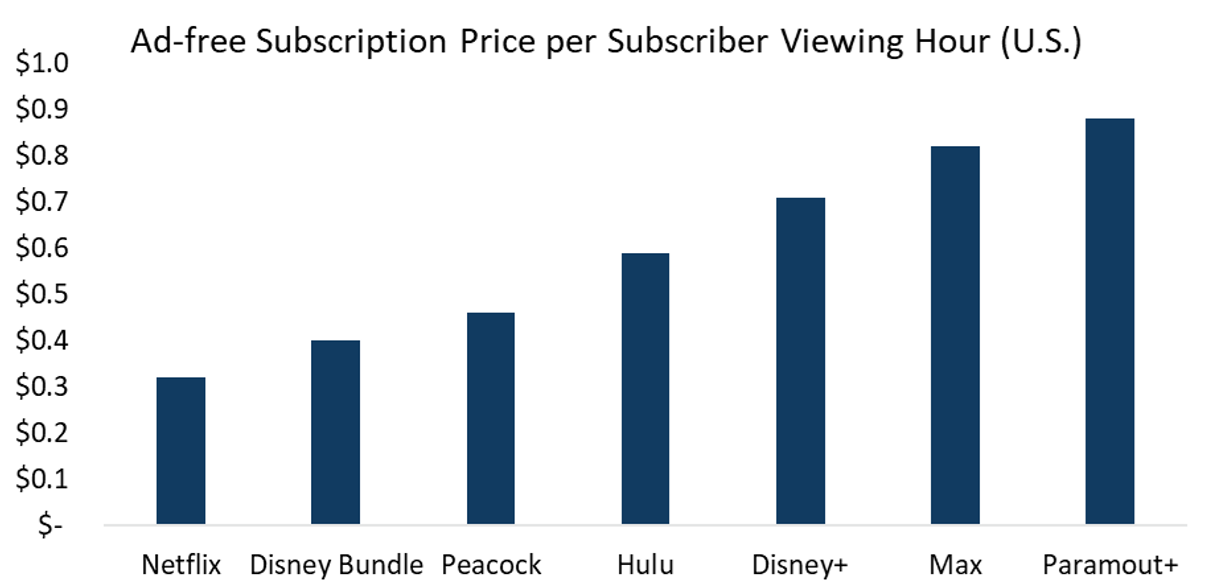

Within the U.S., an ad-free Netflix subscription is estimated to cost $0.32 per subscriber viewing hour, meaningfully below other streaming services. Considering further price increases, customers are getting much better value for their Netflix subscription against peers.

Subscription fatigue in the customer base is a risk, however surveys indicate Netflix is the “least likely of the streaming services to get cut” should consumers cancel subscriptions.

With the addition of further quality content and inclusion of periodic live sporting events in the same membership, Netflix is set up well to implement a price increase on its U.S. Standard plan for the first time in three years. A $2 (13%) monthly increase on a Standard plan in the U.S. would produce an estimated 5% upside to current 2025 earnings estimates.

2) Operating expense control

Management expects 2025 revenue growth of 11-13%, with costs growing slower to deliver margin expansion. The vague commentary on cost growth provides a wide range of outcomes and potential earnings leverage.

Consensus expectations sit at 10% operating expense growth for next year. Given the scaled position, we believe it is likely management can control costs tighter than the market expects. If operating costs instead grow at a reasonable 8%, it provides a further 5% upside to consensus earnings estimates.

Netflix – Relative return to MSCI World and Consensus Earnings expectations

In summary, Netflix’s strong content lineup and latent pricing power combined with scope for tighter-than-expected cost control, give us confidence in further earnings upgrades as we move into 2025.